Success, something that must be looked after

February 22, 2017A new look for Swiss catamaran Safram for 2017 season

June 7, 2017

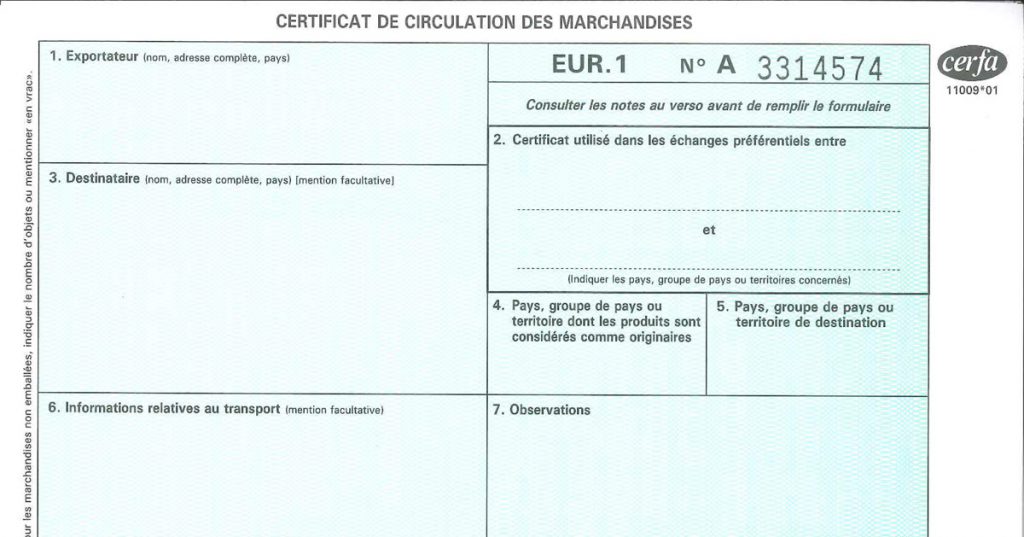

The first step on the way to the end of EUR 1?

The aim is to digitalise customs documents and facilitate customs procedures.

On 1st January 2017 new proofs of origin were introduced in the framework of APS. The new proof of origin replaces the original certificate of origin Form A, EUR 1, and the declaration of origin on an invoice, which was in use to the end of 2016.

The new measure introduces a declaration, which the exporter applies to the trade document, in order to enable the identification of the goods concerned.

ATTENTION: The free trade agreement between the EU and Switzerland is not affected by this.

What are the consequences for exporters?

They vary according to their status: the certificate of origin may be issued by any operator where the value of the originating products in the consignment does not exceed €6,000 but only by a Registered Exporter (RE) if it exceeds this amount.

If the operator is not registered, their products will be subject to full rates of customs duty, leading either to a shortfall for the supplier or high prices for the customer.

It is therefore advisable to obtain the status of Registered Exporter (RE) or Authorized Exporter (AE), which is particularly necessary for South Korea.

Gradual implementation

Self-certification of the origin of the goods is thus becoming the norm, marking the end of the use of EUR.1 certificates – which will nevertheless remain valid for a transitional period of 1 year.

From the 1st January of 2018, it will no longer be possible to have a EUR.1 certificate endorsed at the customs. By the 30th of June 2020, the current proof of origin will be completely replaced by certificates of origin.

Advantages of dematerialisation

Exporters no longer have to submit to the customs a complete technical manufacturing file, for each transaction, proving the Community preferential origin of the goods. The administrative burden and processing times are therefore considerably reduced.

Another advantage is that operators can do without original documents, which can potentially generate errors or get lost when being sent. Finally, remote transmission offers smoother exchanges, both for exporters and for transport providers.

Not to be overlooked

For David Chaillan, Director for Customs and Taxation at Safram, “the dematerialisation of documents is inevitable: it is an opportunity that must not be missed, at the risk of marking the demise of a company operating internationally.”

Indeed, if certain products are subject to full rates of customs duty, “customers will turn to other suppliers, who will have changed their supply chain”. And concludes: “It is essential to start today, because 2018 is tomorrow!”

You can obtain further information from the French customs authority’s website:

http://www.douane.gouv.fr/articles/a12953-nouveaute-dans-le-cadre-du-spg-systeme-rex-et-statut-d-exportateur-enregistre

http://www.douane.gouv.fr/Portals/0/fichiers/professionnel/declaration/spg-systeme-rex-exportateurs.pdf

as well as from that of the Swiss customs authority:

https://www.ezv.admin.ch/ezv/fr/home/infos-pour-entreprises/exonerations–allegements–preferences-tarifaires-et-contributio/exportation-de-suisse/accords-de-libre-echange–origine-preferentielle/REX.html

For further information, please contact the following people at Safram :

– for Switzerland: Mrs Alma Puzic / + 41 22 827 03 44

– for France: Mr David Chaillan / +33 4 72 47 67 09

{kind=link}